What is a Purchase Journal? Example, Journal Entries, and Explained

Crediting the Accounts Payable account increases the company’s liabilities, showing that the purchase will be paid for at a later date, not immediately impacting the company’s cash flow. If the purchase is on credit, credit the Accounts Payable account to increase the company’s liabilities, indicating that the company has an obligation to pay the supplier in the future. When there is only one account debited and one credited, it is called a simple journal entry. There are however instances when more than one account is debited or credited.

- Accounting journals are a great way to break down income and spending into more manageable categories.

- Journal entries are recorded in the “journal”, also known as “books of original entry”.

- Initially, the details of the inventory purchase, including the quantity, price, and terms of sale, are determined.

- In the 1980s, the Times began a two-decade progression to digital technology and launched nytimes.com in 1996.

Journalists

On March 28th, Power Tools purchased office supplies on account from Eco Supplies for $750. Credit purchase of current assets/Non current assets are not considered when recording in Purchase journal. Usually, debits have a left alignment in the entry field while credits are indented or aligned with the right side of the line. This is an easy method for quickly identifying which transactions are deposits, and which ones are withdrawals.

Related AccountingTools Courses

The correspondence accounts that should be recorded included accounts payable, inventories, expenses, and other related accounts. If you make a mistake in your purchases journal, it is important to correct it as soon as possible. You may also want to consider using a software program or online tool to help you track your purchases. This can help eliminate the possibility of mistakes being made in the journal. The Times was founded as the conservative New-York Daily Times in 1851, and came to national recognition in the 1870s with its aggressive coverage of corrupt politician William M. Tweed.

What Is a Purchase Journal? Definition, Format & Example

Businesses often have expense accounts set up to make budgeting easier. You need to note which account funds are taken from to pay for a purchase. Periodically, and no later than the end of each reporting period, the information in the purchases journal is summarized and posted to the general ledger. This means that the purchases stated in the general ledger are only at the most aggregated level. If a person were researching the details of a purchase, it would be necessary to go back to the purchases journal to locate a reference to the source document.

Content management system

The bookkeeper might also decide to add a column with a short description of the purchase details. In addition, you will also see the amount of the invoice and specific accounts that were involved in the transaction. Usually, at the end of the month, the bookkeeper will total the amounts for each account and transfer the total to the Purchases account. Accounting journals tax treatment of self are a great way to break down income and spending into more manageable categories. Purchase journals offer the benefit of tracking and categorizing spending over time to see how a business is spending money. When the time comes to create your annual budget, a purchase journal helps you estimate how much you’ll need in the coming year for various business expenses.

If there is a small number of transactions of credit purchases, then the entity might record the purchase journal together with other transactions. This special journal is prepared for reducing the large of transactions in the general journals. And it is normally prepared only if the entity has a lot of purchases on credit transactions. In the landmark decision New York Times Co. v. United States (1971), the Supreme Court ruled that the First Amendment guaranteed the right to publish the Pentagon Papers. In the 1980s, the Times began a two-decade progression to digital technology and launched nytimes.com in 1996.

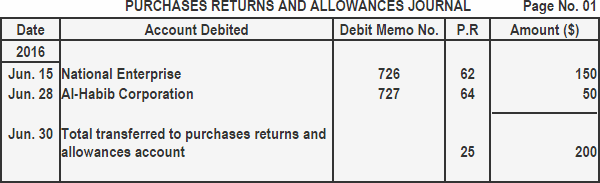

The purchases journal, sometimes referred to as the purchase day book, is a special journal used to record credit purchases. The purchases journal is simply a chronological list of all the purchase invoices and is used to save time, avoid cluttering the general ledger with too much detail, and to allow for segregation of duties. Purchase journals are a vital part of the accounting process of any organization.

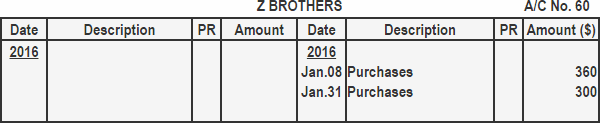

Cash purchases are included in another special journal called the cash disbursements journal, and purchase returns are included in the purchase returns journal or if not used, the general journal. At the end of the period, we would post the totals of $7,650 credit to cash, the $7,500 debit to accounts payable, and the $150 credit to merchandise inventory. The DR (debit) Other column would be handled a little differently as you need to look to the account column to find out where these individual amounts should be posted. In this case, we would post a $200 debit to merchandise inventory and a $300 debit to utility expense. Under the periodic inventory method, the July 6 shipping costs would go to a Transportation In account and the July 25 discount would go to Purchases Discounts. After analyzing and preparing business documents, the transactions are then recorded in the books of the company.